%20(800%20x%20450%20px).avif)

-

30/3/26 4:00 pm

There’s been a sharp fall in investor and commercial occupier sentiment in the last quarter, reflecting the strain of rising debt costs and November Budget uncertainty. Deals are thinning and lenders are turning highly selective in what is now a two-speed market that rewards only quality.

"Animal spirits," a term coined by economist John Maynard Keynes, refers to the psychological and emotional factors, such as confidence, hope, fear, and pessimism, that drive human economic decision-making and are essential for action. Uncertainty puts a huge damper on this.

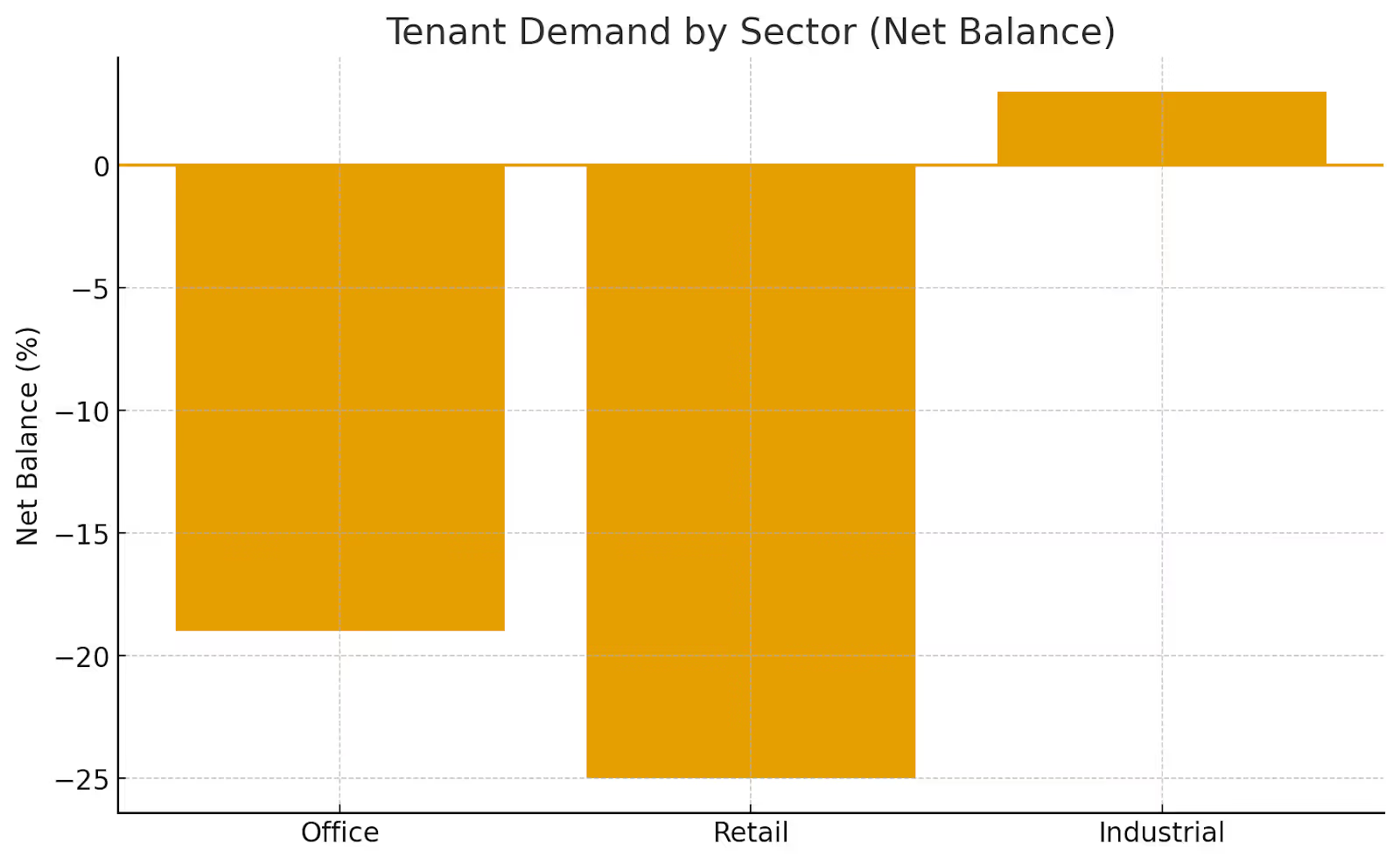

As the UK economy suffers from that vital spark, a severe lack of confidence, according to the latest RICS UK Commercial Property Monitor, both the Occupier Sentiment Index at (–12) and the Investment Sentiment Index at (–10) fell into negative territory in Q3 2025. Tenant demand is sliding, retail is especially a soft market, and credit conditions have tightened for yet another quarter.

These are early signs of a sector losing its way: according to some experts the market has spent two years absorbing higher rates, weaker economic momentum, a slow, patchy return to the office and rapidly increasing home online shopping.

Since Rachel Reeve’s Spring Statement, anxiety over a looming doom-laden Autumn Budget has been adding more risk — enough for many investors to sit firmly on their hands and it’s caused the growth engine to stall.

The RICS report notes that respondents repeatedly flagged government policy uncertainty as the standout reason behind stalled transactions. And with talk of tax rises to come; changes to business rates, and more fiscal tightening, it’s no surprise that sentiment has been sliding.

The numbers are indisputable. The net balance for tenant demand across all commercial sectors fell to –10 per cent, with retail hit hardest at –21 per cent. A net balance of –12 per cent of respondents thought credit conditions had worsened over the period.

Expectations for capital value growth came out broadly flat across the piece for prime assets but were negative for most types of secondary commercial property stock. Landlords are generally having to increase leasing incentives, especially in retail and secondary office markets.

Economics consultancy Capital Economics interprets the RICS survey in similarly sober minded terms, issuing a warning that the combination of fiscal uncertainty, elevated bond yields and expensive debt continues to sap rental and capital growth prospects. A meaningful recovery looks unlikely until policy clarity returns, and until lenders regain confidence in asset resilience.

There is little doubt that Budget anxiety has pulled up the handbrake. Investors are, in the current market, extremely reluctant to commit capital with the possibility of tax reform on the horizon, whether that be to Stamp Duty (SDLT), business rates, capital gains tax, or transaction structures, all possibilities hanging over them.

Small and mid-sized landlords are feeling the pinch even more acutely than the larger institutional investors. They don’t in the main have the same cheap debt, institutional buffers or multi-asset portfolios to diversify their risks. When policy risk rises, they simply cut back on activity first, and the market slows down in response.

This Budget’s outcomes will set the tone for 2026 and beyond. The sector along with most of the rest of this country is now effectively holding its breath ahead of this Budget. Several changes could move markets immediately: Business rates is a favourite as more support or otherwise will ripple directly through retail viability.

Property tax reform following hints of SDLT or CGT changes could have the effect of either freezing or unlocking more deals. Infrastructure spending will have a more long-term impact with investment plans affecting regional office and industrial markets. Green incentives may also offer some financial support for EPC upgrades that might tip the balance of value, adding it back to retrofitted assets.

Budgets have the potential to shift sentiment overnight, whether this does or not remains to be seen but unfortunately going by the experience of the last Budget, people aren’t optimistic. Whether it stabilises the market or knocks it further off-balance will become evident this week.

Gone are the heady days of almost zero interest rates, cheap money available to funnel into assets. Even though the interest rate cycle is expected to ease, lenders have not returned to pre-Covid pricing or risk appetite.

A report from CBRE put the 2025 outlook in perspective when it claims the all-in cost of debt for prime offices at around 5.8 per cent in 2024 has now fallen to only around 4.8 per cent by year end 2025, that’s if more rate cuts materialise. That is still slowing deals. Transaction volumes remain subdued because with many deals the numbers simply don’t stack-up.

Lenders are favouring quality stock for safety. Energy-efficient, well-located, sustainably designed commercial property assets can still attract finance whereas weaker secondary stock cannot.

It’s a two-speed market and a gloomy one at that. It seems there is a widening gap between winners (prime) and the losers (secondary / tertiary) emerging. Prime sustainable offices, logistics sheds, data centres and life-science campuses are all in demand, they remain competitive.

But secondary offices, those older and less well positioned retail units and energy-inefficient stock are drifting into a “value-trap” spiral. The latest office update from Cluttons highlights this trend very clearly: the West End of London is seeing modest capital value growth, while City submarkets face the tailing off of demand and rising vacancy rates.

The divergence is structural. ESG compliance, energy performance (EPC) standards, and location fundamentals are now almost mandatory. Buildings that don’t meet occupier expectations are losing traction fast.

With more space available and weaker economic momentum, occupiers are bargaining harder, they know they can push harder for concessions, incentives, better deals. Retail in particular has seen an increase in lease incentives on offer, longer rent-free periods, flexible lease lengths, and turnover-linked rent structures.

Landlords who fail to adapt to these conditions will lose out. Those who offer smarter, more tailored incentive structures can achieve better long-term rents at the expense of short-term concessions.

While banks and alternative lenders are still active, underwriting is tight. Refinancing windows are getting more challenging for landlords with ageing stock or shorter income profiles. Debt service coverage ratios are biting harder, and lenders are scrutinising ESG compliance more rigorously.

For landlords with 2025–26 refinancing deadlines approaching, now’s the time to get a plan, to prepare updated valuations, to model stressed rental assumptions, to review EPC and compliance risks and to approach lenders early, whatever the Budget fallout brings. Some may need to consider partial disposals, capital investment programmes or equity injections to satisfy lenders’ creditworthiness requirements.

Commercial property confidence is wobbling and the uncertainty during the run up to the Autumn Budget has done nothing but harm to the already structurally weak UK commercial property market.

Many prime assets are holding steady, but secondary stock is under growing pressure. Borrowing is expensive, lenders are selective, tenants have the upper hand, it’s a tenants’ market right now, and policy uncertainty is stopping activity, creativity and risk taking.

However, experience tells us that nothing lasts for ever and oftentimes opportunities stem from adversity. For those landlords who plan ahead, who prepare now by stress-testing cashflows, shoring up debt, and upgrading viable assets will be fine. They will survive and perhaps thrive, whereas others will not be so fortunate. The market isn’t crashing. It’s simply going back to basics, perhaps becoming more honest.

Tags:

.avif)

.avif)

Comments