%20(800%20x%20450%20px).avif)

-

30/3/26 4:00 pm

But don’t let the headline mislead, it must be tempered by a realistic appraisal of the markets.

There’s a real — and measurable — shift underway in the UK commercial property sector. The freeze in investment after 2022 appears to be thawing: earlier cuts to the Bank of England’s bank rate, and a loosening cost of debt, are reopening deals and bringing buyers and lenders back to the table.

That’s good news. But it’s by no means a blanket recovery. For small private landlords who own a shop, parade of retail units, or a single office building, the opportunities are very real — but so are the traps. Here’s a straight-talking, practical view of what’s changing, why it matters, and exactly what you should be doing now. See Rightmove

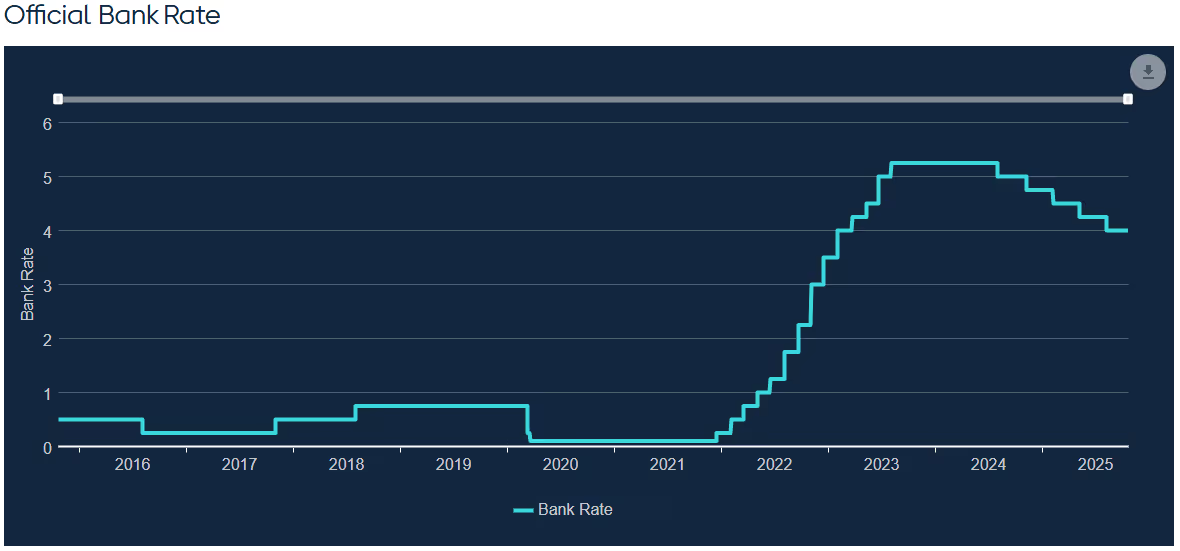

The UK’s bank rate, set by the Bank of England, is currently 4%. It was last held at this level at the September Monetary Policy Committee (MPC) review, and the next decision is scheduled for November 6, 2025. The rate influences other interest rates across the economy, and it is used as a tool by the Bank to both keep inflation stable at or near the government's target of 2% and influence investment.

Investment demand for commercial property has risen year-on-year with Rightmove’s Q2 2025 tracker reporting overall investor demand up around 20%, retail up around 35% and office demand up circa 65%, all compared to a year earlier.

That bounce coincided with the Bank Rate cuts in May and August 2025 from 4.5 per cent down to 4 per cent, while the rate was held at 4 per cent in September. Nevertheless, the drops have eased the full cost of debt for many buyers.

In plain terms, cheaper borrowing makes more deals viable again and narrows the valuation gap between nervous sellers and picky buyers. “If your asset is clear, let’s-call-it ‘bankable’, you’re likely to see more enquiries and firmer offers than you did in 2023–24,” says Rightmove.

The recovery of the retail sector in the UK has continued in the third quarter of the year, according to the latest data from the UK’s number one commercial property website Rightmove.

Demand to invest in retail property, according to the website platform, was up by 30 per cent in Q3 2025 compared to the same period in 2024. The office market is also continuing to recover, with investment demand up by 31 per cent over the same period, and leasing demand up by 7 per cent. Overall demand to invest in commercial property was up by 11 per cent year-on-year in Q3 2025.

The figures build on the momentum from last quarter, where demand to invest in retail property was up by 35 per cent compared with the same three-month period in 2024, while at the same time, supply of retail property fell by 2 per cent.

Rightmove’s MD of Commercial Real Estate, Andy Miles says:

“Bank Rate cuts are supporting investment in the retail sector, and the commercial property sector more broadly compared with last year. The retail sector is also being helped by more realism over values, and an improving occupational market. However, like all aspects of the commercial property market, there are some segments and sectors of the market doing better than others. High-street retail is showing some positive figures overall, but some high streets and shopping centres in secondary locations will be moving more slowly.”

High-street retail investment demand, which makes up a large proportion of the retail sector, was up by 45% compared to the same quarter last year. That is down slightly on the Q2 year on year figure - at 56% - but is nevertheless robust, concludes Rightmove.

There’s renewed interest in investment in the retail sector as a result of multiple factors, most importantly continuing - albeit cautious – the previous cuts to the Bank of England’s Base Rate. The 4% in August was its fifth reduction since August 2024.

Outside of the retail sector, the office market is also continuing a recovery path, with demand to invest in office space up by 31% compared with last year, and demand to lease office space up by 7%. London markets especially have seen big boosts in leasing demand, including Westminster, the City of London, and Hackney.

The industrial sector, the least affected during Covid, continues to lead the way as it has done throughout the year. The latest snapshot of the sector shows that demand to lease industrial space is up by 29% compared with the same period last year, while investment demand is up by 53%.

The Bank of England is cautiously navigating the tricky balancing act between keeping inflation under control while at the same time providing sufficient impetus to the recovery. If inflation bounces back to any great extent, cuts could stall and debt costs could rise again. It can’t be assumed rates will keep falling.

Retail today goes beyond the high street; it is several markets in one. The recovery is strongest for retail parks and convenience/essential retail: grocers, discount anchors and bulky-goods showrooms. Demand there is robust because people still need to buy these items in person. JLL and Savills data show supermarkets and retail-anchored parks outperforming high streets and malls.

Prime high street locations, where footfall is strong and where tourist trade flows or where office catchments have recovered assets are seeing more interest, but pricing is still cautious according to JLL

On the other hand, secondary high streets and stagnant shopping centres are still substantially challenged; with buyers / investors looking for big discounts or redevelopment upside.

Convenience stores and retail-warehouse format units are in the sweet spot. For those owners of tired parades of secondary shops, it’s a different story. The market will only reward these if they can show a realistic tenant uplift, change of use, or redevelopment potential such as commercial to residential. Lower rates won’t work their magic here - buyers price in leasing risk, vacancy, and the cost of capex says Savills.

It’s a similar story with offices. Office demand is rebounding for well-specified, well-located buildings. Grade A stock that meets environmental sustainability credentials, has good floorplates and modern amenities that support hybrid working is in demand.

CBRE’s mid-year outlook report flags improving leasing activity and a return of investor confidence in prime office stock. But secondary offices, those in poor locations, old services, outdated facilities and in need of extensive refubs to meet environmental standards are definitely not back in favour according to CBRE

For small-scale landlords with a single office block, that means two routes: (a) invest to meet market expectations (EV charging, EPC work, flexible floor layouts), (b) accept a longer marketing period and lower price, or plan for conversion where planning allows. There may not be a market to sell “as is” at pre-2022 values says

What to do — a pragmatic approach checklist for the small-scale commercial landlord:

When it comes to letting shorter, flexible lease structures with break options and phased rent reviews are more likely to attract occupiers in secondary locations, than is holding out for long leases.

Tenant mix matters in retail, so tenants that attract footfall, say grocers and service-led anchor tenants, make the rest of a parade a lot easier to let. Providing incentives may be necessary but being surgical as opposed to liberal is a wise approach. A rent-free period or fit-out contributions can unlock a materially longer lease or stronger covenant.

Policy shocks such as business rates changes or permitted development changes could undermine the viability of any repurposing scheme. The threat of a severe recession, stamp duty changes or inflation rises will have buyers disappearing very quickly. Always have a contingency plan.

Lower rates have reopened the market for investors and improved sentiment in retail and office markets, but the recovery is selective. For owners of the “right” types of retail property and good high-quality office space in strong locations, expect more buyers and firmer pricing.

For secondary, either invest to reposition it to today’s occupier expectations or be honest about time and price. For small landlords, the winning play is straightforward: sort your finances, prioritise capital expenditure that preserves or increases rent, and price realistically if you want to sell quickly.

[Main image credit: Ollie Craig]

Tags:

.avif)

.avif)

Comments