%20(800%20x%20450%20px).avif)

-

30/3/26 4:00 pm

Political instability and regulatory headwinds have dented the UK’s commercial real estate attractiveness.

According to Investec, the warning comes from leading investors with £300bn+ in assets under management, while small-scale property investors are doubling down on their threat to leave the private rented sector.

Global institutional investors are no longer queuing up to pile into UK commercial property the way they once did. A recent Investec survey of 50 global institutional investors representing more than £300 billion of assets under management finds that political uncertainty, regulatory churn and the spectre of “higher for longer” interest rates are weighing heavily on sentiment – November 2025 Budget OBR forecasts long-term bank rate and bond yields revised upwards - see below:

Even though some sectors retain their appeal, the overall message is stark: policy churn is imposing a brake on deal-making and altering where and how capital is deployed.

This isn’t a classical capital flight, says Investec, it’s more of a selective, patient reallocation of capital away from the UK. Investors are staying away from exposure that looks sensitive to policy changes or are legally risky, while doubling down where the fundamentals stack up, where demographic demand for homes or the structural need for logistics space remain solid.

At the same time, similar contrast applies to the private rented sector, change and uncertainty and high tax rates are acting as a deterrent to the traditional small-scale buy-to-let landlord.

After months of an unprecedented and exhausting speculative period prior to the Autumn Budget, policy kite-flying and last-minute U-turns rattled the markets. When Rachel Reeves finally unveiled her much-anticipated second Budget, delivered as late in the year as politically possible, the response was mixed.

City officials focused on the challenge of financial stability amid funding pressures, while property investors reacted cautiously to the new tax measures that could impact profitability, and especially a reduction in small-scale investors’ income.

The Chancellor faced a tough backdrop to her second Budget with stagnant economic growth (GDP), persistently high inflation, rising unemployment and interest rates that continue to squeeze both UK households and businesses.

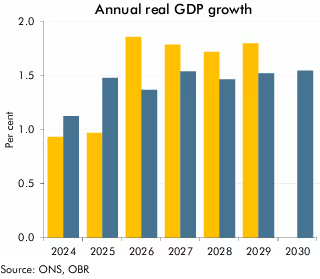

OBR, UK GDP growth revised down since the March forecasts show flatlining and anaemic UK growth for the foreseeable future:

- Yellow bars are the March 2025 forecast

- Blue bars are for November 2025

Welfare spending is rising, and a fiscal black hole is widening, and Labour puts welfare spending high on its list of priorities, so Reeves has opted for a mix of stealth and structural tax measures to raise revenue. The Budget relies heavily on three-year frozen tax thresholds, higher property-related taxes and another step on the direction of wealth taxation.

The result for the UK is most likely a further short-term cooling in business activity, a repricing of secondary assets and an ongoing premium for prime property with clean legal title. (Estates Gazette)

The extra 2 per cent on rental property, dividends and saving income, and the levy on tourism for overnight stays on individual small-scale landlords with short-term lets, came as a major disappointment given that landlords already consider themselves overtaxed. The 2 per cent increases will raise rates to 22 per cent, and 47 per cent for additional rate taxpayers.

Hargreaves Lansdown head of personal finance, Sarah Coles has commented elsewhere:

“Property investment has always come with a painful tax bill. This announcement intensifies it. Landlords pay tax on the way in, tax on the sale, and tax on any income along the way. The hike in the tax rates on rental income makes things even worse. Property investors might have to reconsider whether the maths still adds up under these rules, or whether they should join the exodus from the sector."

Investec’s Future Living 4 research canvassed 50 global institutional investors who collectively manage more than £300bn. The findings are blunt: three-quarters of respondents say political uncertainty is undermining the UK’s appeal, and a significant proportion point to regulatory pressures.

The Building Safety regime is having a major impact. As a deterrent for investment in high-rise and legacy assets it couldn’t have had a greater impact. At the same time however, a large majority of investors expect to maintain or even increase allocations of capital into the living (Build-to-Rent) sector over the coming five years.

The survey shows that while headline demand for UK assets remains, where policy is unclear, deals will stall; where legal liability is opaque, capital requires a higher return. That combination widens bid–ask spreads and pushes transactions toward prime, well-documented assets, says Investec.

For “Political instability” read unpredictable tax and regulatory interventions, last-minute Budget surprises and an uncertain timetable for major reforms. Headlines over business rates, sudden consultations on lease reform and swift legislative responses to building safety problems have created a perception that the rules of the game can change at any time, mid-play development. This degree of uncertainty matters when it comes to capital allocated for real estate investments.

The consequences are all too familiar: lenders become more cautious or more expensive for marginal assets, sponsors face tougher underwriting questions, and managers increase due diligence on remediation (cladding, fire risk) exposures and lease covenants. In short, the cost of holding and trading certain assets rises. That’s the mechanism by which policy noise converts quickly into valuation risk.

The Building Safety Act is reshaping the risk profile for higher-risk, generally high-rise, buildings. Recent tribunal decisions and the increasing value of remediation bills mean that many institutional investors have a reduced appetite for high-rise or complex mixed-use assets until the liabilities with these become clear. The short-term effect is a reduction in the value of buildings, especially secondary stock with remediation (cladding and fire) risk.

The Government is currently in consultation on proposals around lease reform, rent-review mechanisms and security of tenure. These threatened changes have the potential to change the stability and predictability of income flows.

If rent-review regimes are changed or security of tenure is tightened materially, the present value of long-dated income streams will be affected. This will hit the small-scale landlords with lettings in the secondary retail sector. Investors have a right to be nervous until transitional these arrangements are clarified, says Estates Gazette.

While the Government says it is delivering on its commitment to rebalance the business rates system in England, by introducing permanently lower tax rates for retail, hospitality and leisure (RHL) properties, worth nearly £900 million a year, the chancellor has introduced a measure to target online retailers with large warehouse premises.

This is supermarkets, wholesalers and discount retailers, premises likely to bear the brunt of rising costs, as most of their property portfolios will exceed the £500,000 rateable value threshold. As these increases inevitably get passed on, these measures ultimately could be inflationary.

Under the changes put forward in the Budget, the small business RHL multiplier will now be 38.2p with the standard multiplier 43p in 2026-27. For larger value properties it will increase to 50.8p.

While reliefs will help some occupiers, the complexity of changes and their distributional effects will create winners and losers leading again to uncertainty in capital allocation decisions.

The Renters' Rights Act introduces significant changes for buy-to-let landlords. This new legislation which comes into force fully next May presents both challenges and potential opportunities by increasing regulations, altering tenancy structures, and ending "no-fault" evictions. Landlords will face new costs and a shift toward more professional, business-like operations, while some may leave the market. Those who adapt could potentially find opportunities in the changing market.

The Build-to-Rent sector remains healthy for structural demand. Investec’s survey shows most institutional investors expect to maintain or increase allocations into living over the next five years — the combination of household formation, rental demand and under-supply is a powerful draw.

Investors who are prepared to accept long leases and residential cash flows still see attractive risk-adjusted returns, even if they tighten underwriting around remediation and planning risk according to Investec.

Logistics is another area that retains strong support. Fundamental demand from e-commerce, low vacancy and yield compression in prime stock mean capital continues to flow here — the usual “safe haven” for core-plus allocations. CBRE’s market commentary points to solid occupational fundamentals that underpin investor interest despite macro noise.

The office market splits between prime central business district offices which are well-located, ESG-compliant and with strong tenant covenants will still command capital investment. Secondary property stock with poor ESG credentials or weak occupier demand faces a tougher time and greater repricing. The result is a two-tier market with winners (prime) and losers (secondary). (CBRE)

Retail & leisure outcomes depend very much on location. Flagship retail in strong locations may continue to attract bidding from specialised investment funds, while large parts of the convenience and high-street universe remain sensitive to business-rate treatment and changing consumer behaviour. Business rates support does not remove structural headwinds.

The November 2025 UK Budget introduced significant tax increases for landlords, including those with Houses in Multiple Occupation (HMOs), holiday lets and Airbnb style short-term lettings and it highlighted an increase in regulatory burdens and operational costs.

The Investec survey is a reality check for the commercial property sector. Although the UK retains many strengths the country has a problem of perception. Political churn, poor signalling on regulatory changes and unresolved liability questions are imposing a measurable cost on capital investment.

Investec says that if the next 12 months can deliver clearer rules and fair transitional arrangements, the queue of waiting £300bn-plus of institutional capital will flow — and quickly.

Until then, the commercial market will look like a two-speed economy: premium pricing for clean, modern prime assets and steep discounts for anything with legal or policy tail-risk.

As for the private rented sector, for smaller landlords there’s considerable uncertainty in anticipation of the implementation of the Renters Rights Act next May. Considerably more administrative work will be entailed in legally renting out property. Add to this the relentless increase in the tax burden and is it any wonder that many landlords are considering their position?

[Main image credit: Nancy Bourque]

Tags:

.avif)

.avif)

Comments