Akiva worked in the charity sector and property management before joining the legal team at Landlord Action. He has helped countless landlords get back possession of their property from some of the most difficult tenants.”

Alex Nolan, Senior Training Manager at NRLA, provides expert training on HMO management, tenancy processes, and rental sector legislative updates.

Alphaletz is designed to be a simple, cost-effective solution to these problems. Their mission is to free you from the burden of spreadsheets and paperwork, so you can free up time and keep an eye on your profits.

Partner at Xeinadin. Xeinadin is a leading provider of accountancy services and business advice for small and medium-sized enterprises and individuals across the UK and Ireland.

Established in 1860 to care for abandoned animals, Battersea aims to never turn away a dog or cat in need of help. In 2023, we helped 2,529 dogs and 2,450 cats across our three centres. Our work means we see day-to-day the many animal welfare issues facing dogs, cats and the people who care for them.

With over 170 locally-managed offices of letting and estate agents nationwide, Belvoir can provide you with the best service and advice to suit your needs

Ben is the Chief Executive of the NRLA. Prior to taking up his position at the NRLA, Ben was the operations director at Touchstone, part of the Places for People housing group, and was also the managing director of a leading deposit scheme in Northern Ireland. Ben is also a landlord.

David Coughlin is a Cambridge University graduate with more than 20 years’ experience trading property across the UK. Known for maximising and reinvesting capital gains, he has built a substantial property portfolio and is widely regarded as a leading figure in the UK property sector. He has been recognised by the press as one of the UK’s most successful businesspeople and entrepreneurs, noted for both the scale of his property interests and his long-term, strategic approach to the market. David played a key role in raising standards within the quick house sales sector. He was a founding member of the National Association of Property Buyers, working in consultation with The Property Ombudsman to help establish best-practice guidelines for the industry. His stated aim is to challenge traditional approaches and reshape how property is bought and sold in the UK, with a focus on transparency, professionalism, and better outcomes for all parties involved.

CEO of Hamilton Fraser

The HFIS group started as a niche insurance broker focused on the private rented and aesthetic sectors in 1996. Now an established company of over 11 brands and services to the industry, the HFIS group includes Total Landlord, six time award winner of ‘Best Landlord Insurance Provider’ and Hamilton Fraser, ‘Best Specialist Insurance Provider 2023’. Over the years, they have grown to include government authorised schemes such as mydeposits and targeted acquisitions, extending our roots through partnerships with trade bodies and regulatory organisations.

Helen has been writing about property for many years and as well as writing for LandlordZONE and other property industry titles, has worked for Trinity Mirror’s local newspapers, and started her career at the Brighton Argus.

Kim has a strong background in the lettings industry, having worked in Property Management since 1999. Starting out as a Property Manager, she then worked her way through the ranks, spending several years at Countrywide Plc, before receiving her promotion to Director of Property Management and joining Romans in 2018. Now as Group Director of Property Management for LRG, Kim oversees the running of a large, national team who serve circa 60,000 tenancies across the UK, whilst developing the division’s range of services for new and existing customers.

The Landlord Sales Agency retains unrivalled experience in the landlord property sales industry having purchased over 300 buy to let properties over the last 15 years. Their expert knowledge provides them with a unique understanding of the challenges you face, both in running your properties and selling a property portfolio.

Since 1999, LandlordZONE® has been the UK’s leading landlord website, providing property news, advice, legal information and insight for the rental property industry. With over 60,000 members worldwide, LandlordZONE brings an online community of landlords and agents together and provides them with a forum for public discussion on the latest property news. Supporting the journey of a landlord is at the heart of what we do – the website provides free access to comprehensive, educational and reliable information that landlords can utilise throughout their landlord journey. We are dedicated to the publication of unbiased and factual news reporting, working with various property professionals to create a trustworthy, professional and respected community for anyone interested in property.

Leaders is one of the UK's premier estate and letting agents, with more than 100 branches across the country offering a host of property services.

MFB is an award-winning mortgage broker covering all areas of property finance, including buy to let, commercial, and homebuyer mortgages, as well as development and short-term finance. With over 33 years of experience, our team’s knowledge and expertise are unrivalled, making us the broker you can trust. We pride ourselves on our 4.9-star Trustpilot rating and strive to deliver excellence for every single client. When you work with MFB, we take the stress out of your mortgage application process. As a whole-of-market mortgage broker, we’ll find you the best rate for your needs, giving you confidence in your property finance decisions. We proudly recommend MFB as LandlordZONE's official Mortgage Broker Partner, recognising its expertise in the field.

Maria is a journalist who oversees the operations of LandlordZONE behind the scenes, producing news articles and content focused on the private renter sector. She delivers clear, well-researched, and engaging stories that connect with a wide audience, working alongside editor Nigel Lewis.

Michael Lever is a commercial property specialist with a career spanning more than five decades, with particular expertise in rent reviews, lease renewals, business tenancies, and shop property. Educated at the City of London School, he began his professional career in 1967 at Montagu Evans in London before joining his late father’s firm, Fineman Lever & Company, chartered surveyors, in 1971. In 1975, Michael established his own practice, pioneering a specialist focus on rent review and lease renewal work. Originally based in Harrow, North West London, he later relocated his office to Ledbury, Herefordshire, while continuing to advise on properties primarily across London, the South East, and North West England. Alongside client work, Michael has made a longstanding contribution to professional practice and market understanding through extensive writing on rent reviews, business tenancies, and commercial property. Since the late 1970s, he has published a series of influential pamphlets and booklets on rent review methodology, negotiation psychology, auctions, and retail investment, many of which have been widely cited and adopted across the profession. His work has been referenced in legal texts and academic commentary, reflecting its impact on industry thinking. Michael’s writing and commentary have appeared in leading property, legal, and business publications, including the Financial Times, Estates Gazette, Property Week, Retail Week, Investor’s Chronicle, and professional journals serving solicitors, surveyors, and arbitrators. In 1995, he was awarded a prize for an essay on the future of town centres and retailing in a competition sponsored by Marks & Spencer, and in 1996 he received a Certificate of Academic Standing from the The Law Society. He has also served as a guest editor and contributor across a range of professional platforms and newsletters, and since 2022 has written regularly for the LandlordZONE monthly newsletter and contributed to its commercial property forum. Michael is known for a tailored, analytical approach to rent reviews, combining technical expertise with commercial insight. His services are frequently recommended by chartered surveyors, solicitors, accountants, and business advisers, and many clients have worked with him on a long-term basis.

The National Landlord Investment Show is the UK’s Number One landlord & property investment exhibition. Our shows connect thousands of landlords, investors & property professionals and are a beacon for anyone with an interest in buy-to-let or the private rented sector. We have everything you could conceivably need as a landlord or potential investor, including Legal Advice, Finance Suppliers, Investment Opportunities, Tax Experts, Property Management, Education & Mentoring, Proptech, Furnishings / Decor and myriad other helpful services.

CEO of the UK's largest franchised property inventory management and property compliance reporting company - No Letting Go and CEO of Kaptur Software, mobile data collecting software for the property industry. A passionate supporter of the property industry. Previously developed the largest and most successful RE/MAX estate and letting agency in Kent and co-founded Search24 a specialist conveyancing search reports business.

Nigel Lewis is a property journalist and editor with more than 25 years’ experience across national newspapers, magazines and online media. He has worked on a variety of titles, including the Daily Mail, and has edited Channel 4’s A Place in the Sun and Location, Location, Location magazines. From December 2019 to January 2026, Nigel led content at LandlordZONE. His previous senior roles include head of content positions at PrimeLocation and Zoopla, and he has appeared on TV and radio including the BBC, LBC and Radio 5 Live. He writes and edits property content for a range of platforms, with a focus on the private rented sector.

Paul Shamplina is the founder of Landlord Action.

We are a consumer redress scheme, authorised by the Government since 2014, to provide an impartial service that considers consumer complaints about a variety of property related issues. All property agents who carry out estate, lettings and property management work, have a legal responsibility to belong to a redress scheme and, if at any point, the consumer feels the service one of our members has provided falls short of what is expected, they may be able to raise a complaint. We also provide redress for other property professionals which includes landlords, and we offer dedicated tenancy mediation helping to resolve tenancy issues and prevent cases needing to go to court. Please note the Property Redress Scheme is not a regulator or an enforcement agency.

RWInvest is an award-winning property investment company with over 17 years of industry experience and an extensive track record of successfully completed housing projects.

Ryan Shaban is a skilled paralegal at Landlord Action with a strong background in civil litigation and property law. He has successfully navigated contentious disputes, including possession claims and debt recovery. Along with experience in the property licensing sector, he has developed a sharp understanding of property regulations and legislation. Currently en route to qualifying as a solicitor, Ryan offers insightful perspectives on the evolving landscape of property law.

Sean Hooker is the Head of Redress at Property Redress. He is a Qualified Adjudicator (ACIArb), CEDR Accredited Mediator and has a Professional Award in Ombudsman and Complaints Handling Practice (Queen Margaret University and Ombudsman Association).

In-depth knowledge of tenancy deposit schemes, end of tenancy deposit resolution and complaint handling. With over 11 years in the industry and an understanding of some of the challenges faced by landlords, agents and tenants my training focuses on best practice evidence for negotiation, early resolution and adjudication.

I have been a qualified solicitor since 2010 and have worked with HFIS since 2012. With nearly two decades of experience in the lettings industry, I oversee the day-to-day operations of several key schemes at HFIS, including the mydeposits tenancy deposit protection scheme, Property Redress - the government-authorised consumer redress scheme for sales, lettings, and property management agents, and Client Money Protect, the largest client money protection scheme for independent property agents. Throughout my career, I have worked at the forefront of the significant regulatory and industry changes that have shaped the lettings sector over the past decade.

Having built up a small portfolio of these properties he managed them alongside his full-time career in further and higher education. Tom subsequently founded the first landlord website in the UK back in 1999 – LandlordZONE – and is also a recognised writer on the subject of residential and commercial property. Tom has been a regular contributor to real estate journals, blogs, and a speaker at property events for nearly 20 years and now spends his time researching and writing articles for LandlordZONE. He is also regularly quoted in articles.

Starting as an insurance broker in 1996 specialising in property and medical indemnity insurance, these two sectors remain at the heart of everything Total Landlord does. With over 25 years’ experience, Total Landlord continues to raise industry standards, deliver outstanding customer service, and find innovative and practical solutions for their customers’ unique needs. Total Landlord have always been there to help to support the things that matter most and provide a lifetime partnership with our customers.

mydeposits was founded in 2007, giving landlords, agents and tenants an alternative to the other two deposit protection schemes. Now, over a decade later, mydeposits are proud to still giving you a choice by offering all two types of deposit protection, insured and custodial.

The Decent Homes Standard has been labelled as not fit for purpose after private landlords were told they had to comply by 2035.

London Fire Brigade wants landlords to spread awareness of risks around e-bikes and e-scooters after they sparked 206 fires in the capital last year.

Landlord petition tops 13,600 signatures calling for stronger protections as landlords prepare for tougher regulation in the PRS.

A new app aims to transform the way investors source, assess and buy properties.

A complex leasehold redress system is deterring leaseholders from making complaints, according to research by the Leasehold Advisory Service.

The proportion of rental homes sold in Scotland remaining in the private rented sector has nearly doubled over the past year.

Buy-to-let landlords are now incorporating at a rate not seen for a decade, what are the benefits?

South Wales landlord and property investor Mandy St John Davey has been named as one of the world’s top 10 self-made women entrepreneurs.

Landlords are being penalised for housing breaches under both primary legislation and as a breach of licence conditions, says expert.

The rental market continues to cool, with UK rent inflation slowing to its lowest annual rate since March 2022, according to ONS data.

Possession claims are slower and more complex; landlords must prepare carefully, manage risk, and expect longer repossession timelines.

A rogue landlord has failed to have his £26,486 fine for letting two unlicensed HMOs overturned.

Complying with the Renters’ Rights Act will be more difficult for landlords who live overseas, the capital’s watchdog has been told.

Former rentals accounted for 10% of new sales listings in January - down from 17% a year ago – according to new figures.

Rotherham Council is to ask landlords how it should spend £500,000 to improve its selective licensing areas in the town.

Wandsworth Council has launched a crackdown on landlords whose properties don’t meet energy efficiency standards.

Up to 80% of all new buy-to-let purchases are now made via a company, with 66,587 new firms formed in 2025 – up 8% on 2024.

The Government has issued new guidelines you should be familiar with on evicting tenants on or after 1 May 2026, when the Act comes into force

Westminster Council has more than doubled the size of its private renters’ team since launching its selective licensing scheme last November.

Letting agents have warned that proposed guidelines for short lets in Northern Ireland could make it harder for landlords to rent out homes.

The North West has the highest share of HMOs in the UK while landlords in the North East can expect the best yields.

Great Yarmouth landlords have demanded that the local council defend its upcoming selective licensing scheme or face a judicial review.

Ministry of Justice figures reveal a widening gap between falling possession claim volumes and rising court delays, says Landlord Action.

MPs want short let landlords to provide details about the number of nights they let out their properties in a bid to regulate the sector.

Landlords in the private rental sector (PRS) are now being harshly judged by the AML rules – the Government has said it is determined to crack down

The government has been urged to raise the tax-free threshold and incentivise more under-occupied households to rent out rooms to lodgers.

A property lawyer has warned landlords not to accept services in lieu of rent to get round the Renters’ Rights Act.

The Renters’ Rights Act is likely to raise rents and reduce choice by increasing landlords' costs and risks, finds a new report.

Gateshead Council has joined a new national pilot that gives it access to DWP’s secure customer information system.

Hammersmith & Fulham has become the latest council to introduce an Article 4 Direction in a bid to clamp down on HMO conversions.

Tenant death doesn’t end a tenancy. Notice is required, succession may apply, and errors can invalidate possession for landlords.

A new online market rent calculator aims to support landlords and tenants in rent negotiations once the Renters’ Rights Act comes in.

Justice for Tenants is on a mission to create a fairer playing field in the PRS by setting up a legal firm enforcing fines for non-paying landlords.

The government wants landlord leaseholders to share their experiences as it refines the draft Commonhold and Leasehold Reform Bill.

Leasehold reform aims to simplify disputes, empower leaseholders, and reshape property ownership for a fairer, clearer system.

Landlords are being encouraged to sign a new petition calling for revised eviction grounds and more support to weed out problem tenants.

Governments have committed to reforming the leasehold system, but progress has been slow - what does it mean for landlords with leases?

From 1 May, landlords must provide compliant written tenancy terms, with penalties up to £4,000 for missing the 31 May deadline.

Rising taxes, MTD and frozen thresholds mean proactive tax planning is now essential for landlords to protect profits and returns.

Propertymark has set up an independent regulatory board in a bid to foster professionalism, transparency and public trust.

Landlords exiting? We deliver fast, realistic sales of tenanted properties—no refurbs, chain-free buyers and quick completion.

Sefton and Preston councils join other local authorities launching Article 4 directions in a bid to stem the growth of HMOs.

Two thirds of landlords planning to increase rents blame upcoming property tax rises, according to a new poll.

Politicians have backed a proposal to set separate Welsh rates of property income tax, despite fears it could deter investment.

The Bank of England has held UK interest rates at 3.75% but signalled that a cut could soon be on the way.

Landlords could end up with a £1,000 bill for failing to keep their email address updated under new Making Tax Digital rules.

The Renters’ Rights Act is no longer a distant vision on the horizon; it’s a looming reality

Both tenants and landlords are losing out to firms chasing lucrative housing disrepair claims, according to Landlord Licensing & Defence.

A legal expert has advised landlords to beef up their record-keeping to avoid enforcement action under the Renters' Rights Act.

Almost four in 10 landlords plan to refinance property during the next 12 months as thousands of five-year fixed-rate mortgages mature.

Landlords and agents have urged the government to announce commercial EPC deadlines before buildings across major cities become unlettable.

Luton Council has won its long-running legal battle to go ahead with selective and additional licensing schemes in the town.

Bolton Council has launched a consultation into plans for a borough-wide additional licensing scheme.

Leasehold reforms will cap ground rents, ban new leasehold flats, and allow conversions to commonhold, reshaping landlord income streams.

Landlords in England are being asked to help test the new PRS Database, which is being introduced later this year.

The government’s conviction that larger landlords will simply replace smaller landlords could backfire, says a property lawyer.

The Green party has called for mayors to be given the power to set rent controls in a bid to stem renters’ spiralling costs.

Compliance is unavoidable, but rising fees expose which agents are efficient and which are passing their own risk to landlords.

It is possible to turn a utilities supply cost headache in multi-occupied properties into a smoothly managed system

Energy efficiency standards are improving in the PRS while there are also more rented properties meeting decent home standards.

The Renters’ Rights Act could unintentionally force hundreds of thousands of renters to pay stamp duty, according to an investigative group.

Rumble with the Agents returns to London 11 June 2026, bringing the property industry together for charity boxing for North London Hospice.

A Reform UK council chair has resigned after he was named as a 'rogue landlord' who had rented out two dangerous HMOs.

Very few corporate landlords are being penalised for housing offences compared to their smaller counterparts, according to a new study.

Specialist lender Somo has launched a Landlord’s Breathing Space Loan to help investors facing cashflow stress.

Landlords in the Republic of Ireland face tough new reforms that go much further than England’s Renters’ Rights Act.

Two-year delay offers landlords a temporary reprieve, but the underlying pressure is still there

Private landlords will have to meet a new Decent Homes Standard in 2035, the government has announced.

Losing Section 21 is set to cause big headaches for HMO landlords dealing with extremes of anti-social behaviour.

Large portfolio landlords could get a new portfolio-based exemption as part of legislative changes to improve PRS energy ratings.

Rental growth in Scotland dipped from 4.4% at the start of last year to just 0.2% by year-end, according to the latest figures.

The number of pet-friendly rental adverts has barely changed in the last year, despite upcoming changes in the Renters’ Rights Act.

The government has announced a cap on ground rents which is set to transform the residential leasehold market.

UK estate agencies face rising fines as HMRC steps up AML enforcement, naming firms that missed registration, controls.

A lettings expert has urged the property sector to back a national housing committee to come up with long-term strategy.

New rules banning discrimination against tenants with children or those receiving benefits will come into force in Wales on 1st June.

A rogue landlord who refused to fix up his two dangerous HMOs has had them shut down by Tamworth Borough Council.

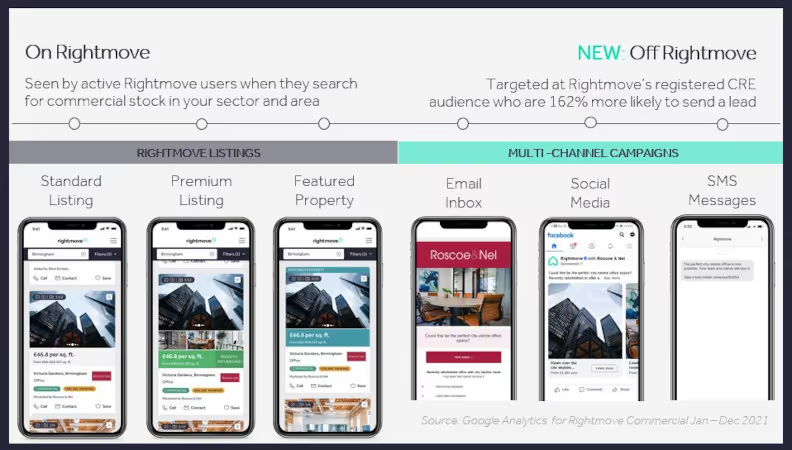

Rightmove’s challenge, and its latest Commercial Property Tracker shows commercial property sector remains positive

Nearly 9 in 10 landlords worry about Making Tax Digital, with many unsure how to prepare ahead of April 2026 rollout.

The industrial sector continued to lead the way for commercial real estate in the UK with demand to lease in Q4 up 11% year on year.

Rents to rise modestly in 2026 as supply improves, demand softens and the Renters’ Rights Act reshapes the lettings market.

The government has insisted tribunals will be ready for an expected increase in rent review hearings after 1st May.

A landlord who let out an unlicensed, mouldy and unsafe home has been told by a court to pay more than £15,000.

With new redress rules coming, landlords should handle concerns early, communicate clearly, keep records and see ombudsman support as protection.

Most landlords appear cautiously optimistic about their portfolios and future investment in the PRS despite tax and regulatory pressures.

Legal experts have warned landlords to be wary of using AI for advice amid reports of tribunal judges finding inaccuracies.

Short let landlords have been told that their properties won’t have to achieve an EPC C by 2030, unlike the rest of the PRS.

Council tax hikes, business rates traps and the real cost of owning a second home or furnish holiday let

Guaranteed rent firm Elliot Leigh has partnered with another eight councils as they look for alternatives to costly nightly paid accommodation.

Landlords in Scotland are to get new timescales on dealing with damp and mould in a bid to better protect tenants in the PRS.

The government has confirmed that all private landlords must get their rental properties up to an EPC C by 1st October 2030.

UK landlords are selling up in record numbers as regulation and rising costs shrink rental supply and intensify pressure on tenants.

Salford Council hopes to crack down on poorly converted HMOs after 99% failed to meet housing and fire safety standards.

New research finds flats and terraced homes saw the strongest gains in yield last year, although HMOs still offer the best returns.

When licensing schemes expire or renew, landlords can face unexpected compliance risks if conditions, fees or designations change.

The government has published details of what landlords must put into tenancy agreements under the Renters’ Rights Act.

Landlords with homes covered by Tandridge Council now face tougher restrictions on converting small HMOs.

Landlords have been warned to be extra careful if trying to find loopholes in the Renters’ Rights Act.

Selective licensing is expanding across England, catching many landlords unaware and increasing compliance risks, costs and penalties.

Just 10.9% of properties in Great Britain were bought by landlords in 2025, down from 12% in 2024, new figures show.

.avif)

%20(1).avif)

%20(1).avif)

.avif)

.avif)

.avif)